Time in the Market vs. Timing the Market: What Retirees Should Know

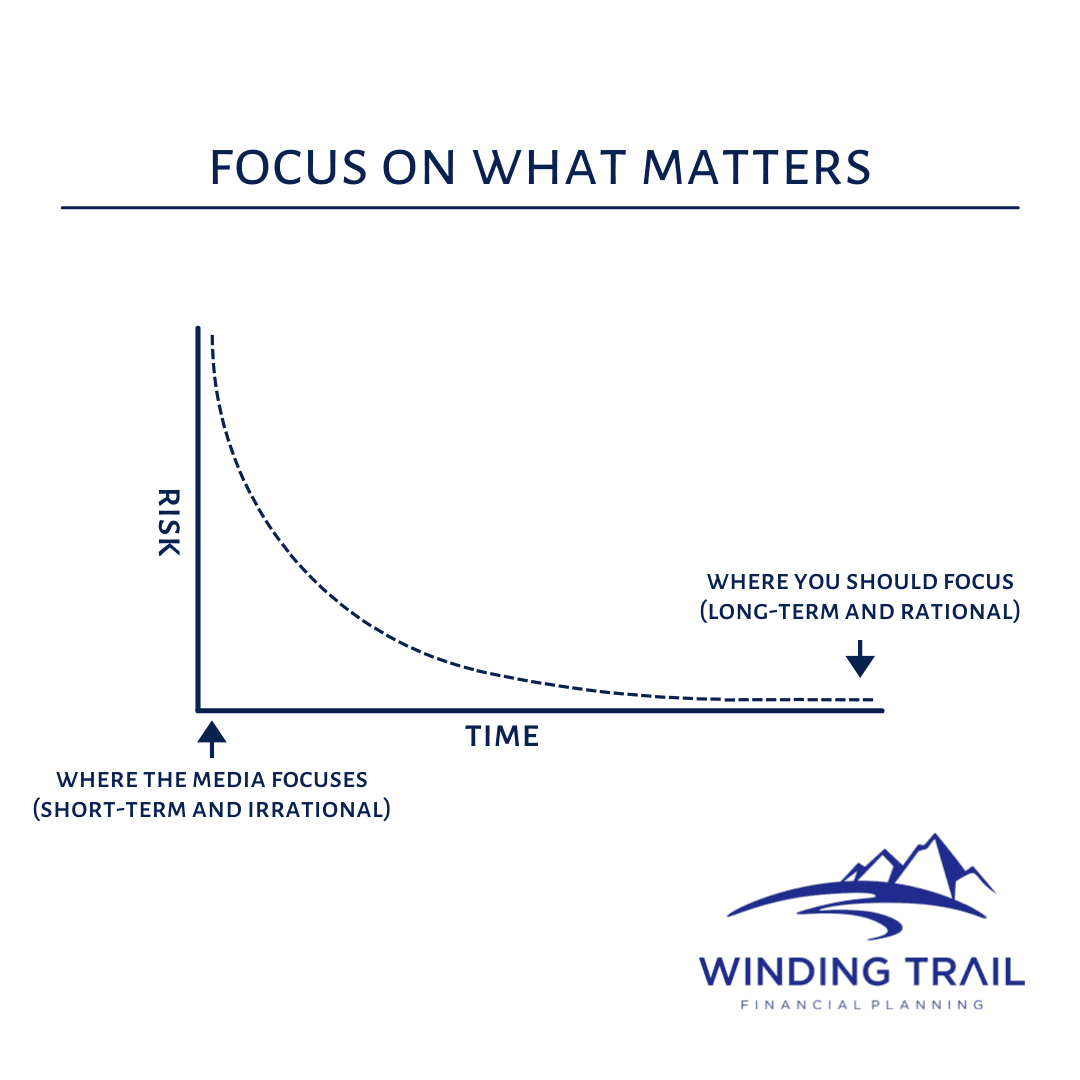

When markets are doing well, it is natural to wonder how long it can last.

When markets are falling, it is natural to wonder whether you should get out before things get worse.

I still remember the Great Recession unfolding while I was in graduate school. My classmates and I were not debating asset allocation theory — we were wondering whether there would be jobs available when we graduated.

At the time, it felt like the financial world had permanently changed. And in some ways, it had. But roughly five years later, the stock market had recovered. Investors who stayed disciplined were eventually rewarded, while many who sold in fear had to figure out when — or whether — to get back in.

That experience is one reason I am cautious when people talk confidently about getting out of the market before things get worse.

And if you remember the Great Recession, the dot-com crash, COVID, inflation headlines, rising interest rates, election cycles, banking scares, or any of the other market-moving events from the last few decades, you may have the same question many investors eventually ask:

Should I try to time the market?

Spoiler alert: probably not.

That does not mean you should ignore risk. It does not mean your portfolio should be on autopilot forever. And it certainly does not mean retirees should invest the same way they did when they were 35.

But for most long-term investors — especially those approaching retirement — the bigger risk is not usually failing to predict the next downturn.

The bigger risk is making a permanent decision in response to temporary fear.

What does “time in the market” mean?

“Time in the market” means staying invested through normal market cycles instead of trying to jump in and out based on predictions, headlines, or gut feelings.

“Timing the market” means trying to sell before downturns and buy back in before recoveries.

That sounds great in theory. The problem is that you have to be right twice.

You have to know when to get out.

Then you have to know when to get back in.

Most investors struggle with both. Not because they are unintelligent, but because market turning points are usually only obvious in hindsight.

By the time things feel safe again, markets may have already recovered significantly.

The behavior gap is the real problem

One of the most important investing lessons is that the return of an investment fund and the return earned by the average investor in that fund are not always the same thing.

That difference is often called the “behavior gap.”

The fund may have produced one return, but the investor may have earned something lower because of when they bought, sold, added money, reduced exposure, or switched strategies.

This is where market timing can become costly.

Investors often sell after markets have already fallen because they are scared. Then they wait to reinvest until the news feels better. Unfortunately, markets do not send an “all clear” signal. Some of the strongest recovery days can happen when the headlines still feel awful.

The result is a painful pattern:

Sell low.

Wait.

Buy back higher.

Repeat.

That is not an investment strategy. That is an emotional response wearing a strategy costume.

Why this matters more as you approach retirement

If you are 30 years from retirement, a market downturn is uncomfortable.

If you are 3 years from retirement, it can feel personal.

The account balance on your statement may no longer feel like a distant number. It may look like your future paycheck.

That shift matters.

When retirement gets closer, the goal is not simply to maximize long-term growth. The goal is to balance several competing needs:

You need growth to help your money last.

You need stability so you are not forced to sell long-term investments during a downturn.

You need liquidity for near-term spending.

You need a tax plan so withdrawals do not create avoidable surprises.

And you need enough confidence in the plan that you do not feel compelled to make major decisions every time the market has a rough week.

This is why retirement investing is not just about picking funds. It is about designing a system you can actually stick with.

The market does not care about your retirement date

One of the hard truths of retirement planning is that the market does not know or care when you plan to retire.

You might retire into a strong market.

You might retire into a bear market.

You might retire into a sideways market where returns are choppy for several years.

This is where “time in the market” needs a little nuance.

A 100% stock portfolio may technically give you more time in the market, but that does not automatically make it appropriate for someone who needs portfolio withdrawals soon. On the other hand, moving everything to cash because retirement is approaching may reduce volatility, but it can create inflation risk and reduce long-term growth.

The better question is not:

“Should I be in or out of the market?”

The better question is:

“What portion of my money needs to be stable for the next few years, and what portion needs to stay invested for the next few decades?”

That is a retirement planning question, not a market prediction question.

Diversification is not the same as owning a lot of things

A diversified portfolio owns investments that behave differently from one another.

That may include U.S. stocks, international stocks, bonds, cash, and other asset classes depending on the situation.

But owning multiple funds does not automatically mean you are diversified.

For example, if you own two or three funds that all track the S&P 500, you may have more line items on your statement, but you may not have meaningfully reduced your risk.

The same applies if you have a large concentration in one company stock, a large position from a long-running bull market, or employer stock that has grown into an outsized part of your net worth.

Diversification is not exciting. It rarely gives you bragging rights at dinner.

But it can help reduce the odds that one company, one sector, one country, or one bad decision drives too much of your retirement outcome.

Your cash flow plan can help you stay invested

One reason investors panic during downturns is that they do not know where their next few years of spending will come from.

This is especially important in retirement.

If every dollar is invested for long-term growth and the market falls, withdrawals can become stressful. You may feel like you are selling at exactly the wrong time.

That is where a retirement cash flow plan can help.

You might hold a reasonable amount of short-term spending in cash or conservative investments. You might use bonds as part of the portfolio. You might coordinate withdrawals from taxable accounts, IRAs, Roth accounts, pensions, Social Security, or part-time income.

The point is not to avoid volatility altogether.

The point is to avoid being forced into bad decisions because you did not plan for volatility ahead of time.

A good retirement income plan gives your long-term investments time to recover while still giving you a practical way to fund life today.

What should you focus on instead of timing the market?

Most investors cannot control market returns.

But you can control a lot more than you may think.

You can control your savings rate while you are still working.

You can control how much cash you keep for short-term needs.

You can control whether your portfolio matches your goals, risk tolerance, and time horizon.

You can control how concentrated your portfolio is.

You can control whether you rebalance.

You can control whether you have a tax-aware withdrawal plan.

You can control how much attention you give to financial headlines.

And most importantly, you can control whether you have a plan before the market tests your patience.

Time in the market still needs a plan

“Time in the market beats timing the market” is a useful saying, but it can be oversimplified.

The goal is not to blindly hold an investment portfolio forever no matter what.

The goal is to build a portfolio and retirement income plan that you can live with through good markets, bad markets, and everything in between.

That usually means accepting that downturns are part of investing.

It means not pretending you can consistently predict the next market move.

It means aligning your portfolio with the actual job your money needs to do.

And it means remembering that investment success is not just about returns. It is also about behavior.

If your plan only works when markets are calm, it is not much of a plan.

Final thought

Market timing is tempting because it offers the illusion of control.

A real plan gives you something better: a disciplined process.

You do not need to know exactly what the market will do next month, next quarter, or next year. You need a portfolio, cash flow strategy, and tax plan that can help you keep moving even when the trail gets rough.

Thanks for reading.

-Dwight

P.S. Winding Trail Financial Planning is a fee-only financial advisor in Lafayette, Colorado. We help retirees and near-retirees make thoughtful decisions about investments, retirement income, taxes, Social Security, and cash flow.

Frequently Asked Questions

Is time in the market really better than timing the market?

For most long-term investors, yes. Timing the market requires you to correctly decide when to sell and when to buy back in. That is extremely difficult to do consistently. Staying invested in a diversified portfolio generally gives you a better chance of participating in long-term market growth.

Should retirees stay invested in the stock market?

Many retirees still need some stock exposure because retirement can last 20, 30, or even 40 years. However, the right amount depends on spending needs, pensions, Social Security, risk tolerance, taxes, and other assets. Retirees usually need a balance between growth, stability, and liquidity.

What is the behavior gap?

The behavior gap is the difference between the return an investment produces and the return investors actually earn because of their buying and selling decisions. Emotional decisions, performance chasing, and panic selling can all widen the gap.

Should I move to cash before a market downturn?

Moving to cash may feel safe in the moment, but it creates another decision: when to reinvest. If markets recover quickly, sitting in cash can cause you to miss part of the rebound. A better approach is usually to build a portfolio and cash reserve that already accounts for market downturns.

How should I invest if I am five years from retirement?

Five years before retirement is a good time to review your portfolio risk, cash needs, tax strategy, Social Security plan, debt, and withdrawal strategy. The goal is not to eliminate risk, but to make sure your money is aligned with the retirement you are preparing for.

Disclaimer: None of the information provided herein is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement, of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. The content is provided ‘as is’ and without warranties, either expressed or implied. Winding Trail Financial Planning, LLC does not promise or guarantee any income or particular result from your use of the information contained herein. Under no circumstances will Winding Trail Financial Planning, LLC be liable for any loss or damage caused by your reliance on the information contained herein. It is your responsibility to evaluate any information, opinion, or other content contained.

Plan Your Next Chapter

Download our free guide "Seven Essentials for Successful Investing in Retirement" and get clarity on what really matters for your retirement success.