Tax-Smart Retirement Withdrawals for Boulder County Retirees

Retirement income planning is not just about deciding how much to withdraw each year. For retirees in Lafayette, Louisville, Erie, Boulder County, and the greater Denver-Boulder area, one of the bigger questions is often which account to draw from first — and how those decisions affect taxes over time.

Many retirees enter retirement with a mix of accounts: traditional IRAs, 401(k)s, Roth IRAs, taxable brokerage accounts, cash reserves, pensions, Social Security, or proceeds from the sale of a business or real estate. Each source of income may be taxed differently. A withdrawal strategy that feels simple in the moment can create unnecessary tax costs later.

That is where tax-smart retirement withdrawal planning comes in.

A well-designed retirement income plan should help answer questions like:

Should I withdraw from my IRA, Roth IRA, brokerage account, or cash first?

Should I do Roth conversions before required minimum distributions begin?

How will Social Security affect my tax bracket?

Could my withdrawals increase Medicare premiums?

Am I managing this year’s tax bill, or my lifetime tax bill?

What happens to the plan when one spouse dies?

There is no single withdrawal order that works for everyone. The right approach depends on your assets, tax bracket, age, income needs, estate goals, charitable plans, and the types of accounts you own.

Why Retirement Withdrawals Are a Tax Planning Issue

During your working years, tax planning often focuses on income, deductions, retirement contributions, business expenses, and investment gains. In retirement, the planning problem changes.

You may have more control over your taxable income than you did while working. That control can be valuable.

For example, one retiree may need $120,000 per year to support their lifestyle. But that does not necessarily mean they need to generate $120,000 of taxable income. Part of the income might come from cash reserves. Part might come from a taxable brokerage account. Part might come from an IRA. Part might come from Social Security. Each source can have a different tax result.

The order and timing of withdrawals can affect:

Federal income taxes

Colorado income taxes

Taxation of Social Security benefits

Medicare IRMAA surcharges

Future required minimum distributions

Roth conversion opportunities

Capital gains taxes

Charitable giving strategies

Surviving spouse tax exposure

Estate planning flexibility

This is why retirement withdrawal planning should not be treated as a simple investment distribution decision. It is a tax planning decision, a cash flow decision, and a long-term financial planning decision.

What Are Tax-Optimized Retirement Withdrawals?

Tax-optimized retirement withdrawals are a coordinated strategy for deciding which accounts to use, how much to withdraw, and when to recognize income.

The goal is not always to pay the lowest tax this year. Sometimes the better objective is to manage your tax bill over many years.

For example, a retiree who avoids IRA withdrawals in their early 60s might enjoy very low taxes for a few years. But if that retiree later has large required minimum distributions, the strategy may simply delay the tax problem. In some cases, intentionally recognizing income earlier through IRA withdrawals or Roth conversions can reduce future tax pressure.

A tax-smart withdrawal strategy may include:

Using taxable brokerage assets strategically before IRA withdrawals

Filling lower tax brackets with planned IRA distributions or Roth conversions

Coordinating withdrawals with Social Security claiming decisions

Managing Medicare IRMAA thresholds

Harvesting capital gains in lower-income years

Preserving Roth IRA assets for later retirement or heirs

Using qualified charitable distributions after age 70½, when appropriate

Planning for the tax impact after the first spouse passes away

The best strategy depends on the household. For some retirees, using taxable assets first makes sense. For others, partial IRA withdrawals or Roth conversions before age 73 may be better. For charitably inclined retirees, preserving IRA assets for qualified charitable distributions may be attractive.

The Common “Default” Withdrawal Strategy

Many retirees follow a default withdrawal order without realizing it:

Spend cash first

Use taxable brokerage assets next

Delay IRA withdrawals until required minimum distributions begin

Preserve Roth IRAs as long as possible

This approach can be reasonable in some cases. It is simple and it may allow tax-deferred accounts to keep growing.

But it can also create problems.

If traditional IRA and 401(k) balances grow too large, future required minimum distributions may push retirees into higher tax brackets. Larger IRA distributions can also increase the taxable portion of Social Security and potentially trigger higher Medicare premiums.

The issue is not that the default strategy is always wrong. The issue is that it is often untested.

A better question is:

What withdrawal strategy creates the best after-tax outcome over the full retirement period?

That answer usually requires year-by-year tax planning, not a rule of thumb.

Roth Conversions Before Required Minimum Distributions

For many retirees, the years between retirement and required minimum distributions can be especially important.

This period may include lower-income years after wages stop but before Social Security, pension income, or RMDs fully begin. Those years can create an opportunity to convert part of a traditional IRA to a Roth IRA at a controlled tax cost.

A Roth conversion means moving money from a pre-tax retirement account into a Roth IRA. The converted amount is generally taxable in the year of conversion, but future qualified Roth IRA withdrawals may be tax-free.

Roth conversions may help:

Reduce future required minimum distributions

Build tax-free retirement assets

Create flexibility later in retirement

Improve tax diversification

Reduce tax pressure for a surviving spouse

Improve after-tax inheritance planning for heirs

But Roth conversions are not automatically beneficial. Converting too much in one year can create avoidable tax costs, increase Medicare premiums, or push income into a higher bracket.

A good Roth conversion strategy is usually not, “Should we convert or not?”

It is more often:

How much should we convert this year, and what tax bracket or income threshold are we trying to manage?

Medicare IRMAA and Retirement Income Planning

Retirees often think about income taxes, but Medicare premiums can also be affected by income.

Medicare uses income-based thresholds to determine whether higher-income retirees pay additional premiums. These surcharges are commonly referred to as IRMAA.

This matters because a withdrawal or Roth conversion that looks good from a tax-bracket perspective may have a second-order effect on Medicare premiums.

That does not mean retirees should always avoid IRMAA. Sometimes paying a temporary surcharge may be acceptable if the long-term tax savings are meaningful. But it should be intentional.

For households in Lafayette, Boulder, Louisville, Erie, Longmont, and surrounding communities, this can become especially relevant when retirement income includes investment assets, deferred compensation, pensions, rental income, or business sale proceeds.

Brokerage Accounts, Capital Gains, and Tax Flexibility

Taxable brokerage accounts can be valuable in retirement because they provide flexibility.

Unlike traditional IRAs, withdrawals from brokerage accounts are not automatically taxed as ordinary income. Instead, the tax impact depends on whether assets are sold, how much gain exists, and whether the gain is short-term or long-term.

A tax-smart retirement withdrawal plan may use brokerage assets to:

Create retirement cash flow without large ordinary income spikes

Harvest long-term capital gains in lower-income years

Harvest losses to offset gains

Coordinate taxable income with Roth conversions

Preserve IRA assets for charitable giving

Preserve Roth assets for later-life flexibility

Brokerage accounts can also receive a step-up in basis at death under current law, which may affect whether it makes sense to sell appreciated assets during life or hold them for heirs.

This is why the best withdrawal strategy is not just about the account type. It is about the tax characteristics of each asset inside each account.

Social Security Timing and Withdrawal Strategy

Social Security is another major part of retirement withdrawal planning.

The timing of Social Security benefits affects how much income you need from your portfolio. It can also affect how much room you have for IRA withdrawals or Roth conversions before your taxable income increases.

Some retirees claim Social Security early and reduce portfolio withdrawals. Others delay Social Security and use portfolio assets to bridge the gap. Neither approach is automatically right or wrong.

The best decision depends on:

Health and longevity expectations

Spousal benefits

Survivor benefits

Portfolio size

Tax bracket

Cash flow needs

Pension income

Roth conversion opportunities

Desire for guaranteed income later in life

For married couples, Social Security planning should also consider the surviving spouse. When one spouse dies, the household generally moves from married filing jointly to single filing status, and one Social Security benefit may disappear. That can create a tighter tax situation for the survivor.

The Surviving Spouse Tax Problem

One of the most overlooked retirement tax issues is what happens after the first spouse dies.

A married couple may have a comfortable tax situation while both spouses are alive. But after the first death, the surviving spouse may have similar income with a less favorable filing status. Required minimum distributions, pension income, Social Security, and investment income can become more compressed into the single tax brackets.

This is one reason partial Roth conversions or earlier IRA distributions may be worth considering during the married years.

The goal is not only to optimize taxes while both spouses are alive. It is also to protect the surviving spouse from being forced into a higher-tax situation later.

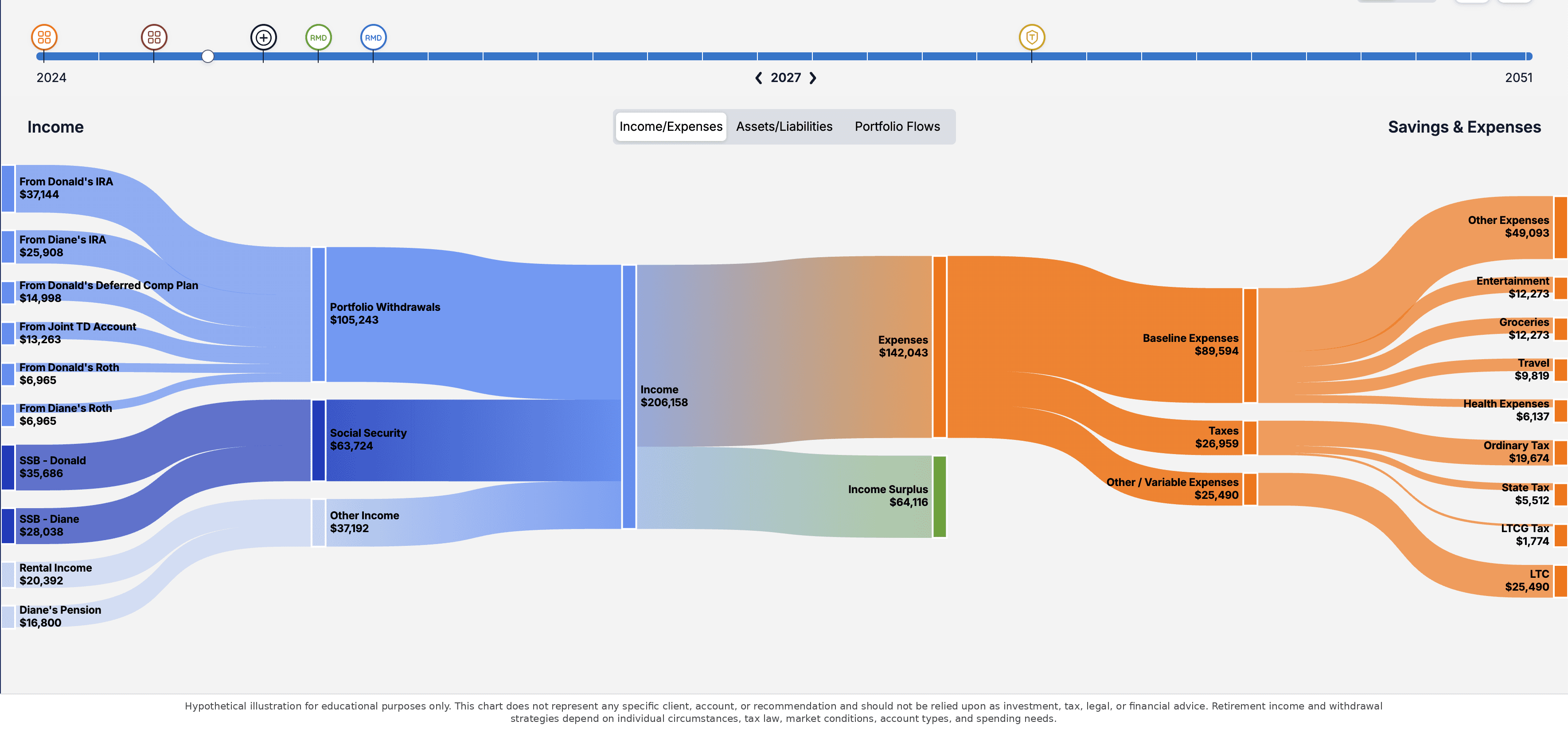

A Simple Example

Consider a hypothetical couple in Boulder County preparing for retirement.

They have:

$1,000,000 in traditional IRAs and 401(k)s

$400,000 in a taxable brokerage account

$200,000 in Roth IRAs

$100,000 in cash reserves

Social Security benefits available in the future

No mortgage

A default strategy might use cash and brokerage assets first, delay Social Security, and avoid IRA withdrawals until required minimum distributions begin.

That could work. But it could also allow the traditional IRA balance to keep growing, creating larger RMDs later.

A more coordinated strategy might intentionally use a mix of brokerage withdrawals, partial IRA distributions, and Roth conversions during lower-income years. The couple might pay some tax earlier, but reduce future RMDs, improve Roth flexibility, and reduce the risk of large taxable income spikes later.

The right answer depends not only on the numbers but also your thoughts on what the future might hold for your and your family given your situation. But the example highlights the central point:

Retirement income planning is not just about where the money is invested. It is also about how and when the money comes out.

Common Retirement Withdrawal Mistakes

Here are several mistakes retirees commonly make when they do not coordinate withdrawals with tax planning.

1. Waiting until RMDs begin to think about IRA taxes

Required minimum distributions can significantly change a retiree’s tax picture. Planning before RMD age may create more options.

2. Assuming Roth conversions are always good or always bad

Roth conversions are a tool. They need to be measured against tax brackets, Medicare premiums, estate goals, and future income projections.

3. Looking only at this year’s tax bill

A strategy that minimizes taxes this year may increase taxes over the next 10, 20, or 30 years.

4. Ignoring Medicare IRMAA

Large IRA withdrawals, Roth conversions, capital gains, or business income can affect Medicare premiums. These thresholds should be part of the planning process.

5. Treating all investment accounts the same

A Roth IRA, traditional IRA, taxable brokerage account, and savings account all have different tax characteristics. Withdrawal order matters.

6. Forgetting about the surviving spouse

The surviving spouse may face higher tax rates after moving to single filing status. Planning during the married years can help reduce that risk. This can be more imperative if there is a sizable age gap or health concerns.

7. Separating investment management from tax planning

Investment decisions and tax decisions are connected. A retirement income plan should coordinate both.

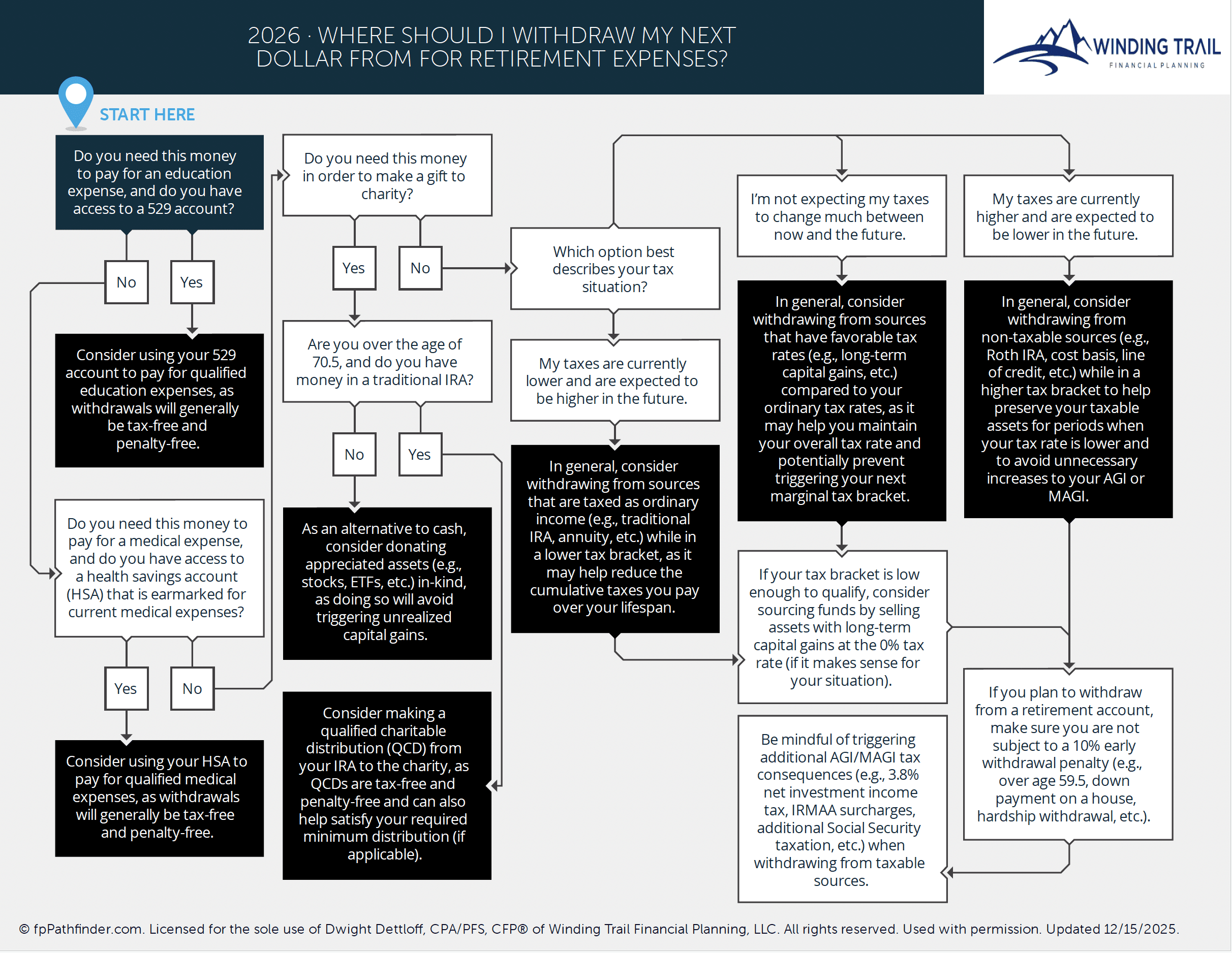

A Helpful Framework: Which Dollar Should Come Out Next?

The decision tree below illustrates why retirement withdrawal planning is rarely as simple as “spend taxable accounts first, then IRAs, then Roth accounts.” The better question is often: what is this dollar being used for, how will it be taxed, and what other income-based consequences could it trigger?

One way to understand retirement withdrawal planning is to stop thinking in terms of a fixed order and instead ask a better question:

Where should the next dollar come from?

That question can lead to very different answers depending on the purpose of the withdrawal, your current tax bracket, your future expected tax bracket, and the type of account available.

For example, money needed for qualified education expenses may point toward a 529 account. Money needed for qualified medical expenses may point toward an HSA. Money intended for charity may point toward appreciated securities or, for IRA owners over age 70½, a qualified charitable distribution. General retirement spending may require comparing IRA distributions, taxable brokerage sales, Roth withdrawals, cash reserves, and other sources. Sometimes delaying a discretionary distribution from one year into another can have a tax impact.

This is where the planning becomes more complex than simply spending one account before another. A retiree in a low tax year may benefit from using ordinary-income sources, such as a traditional IRA, or completing a partial Roth conversion. A retiree in a high tax year may prefer non-taxable or lower-tax sources to avoid increasing adjusted gross income or modified adjusted gross income.

Those income levels can affect more than federal income taxes. They may also affect Medicare IRMAA surcharges, the taxation of Social Security benefits, net investment income tax exposure, capital gains rates, and state income taxes.

A useful withdrawal framework considers:

The purpose of the withdrawal

Whether the withdrawal is taxable, tax-free, or tax-deferred

Whether income is taxed as ordinary income or long-term capital gain

Whether the transaction increases AGI or MAGI

Whether early withdrawal penalties apply

Whether the decision affects Medicare premiums or Social Security taxation

Whether current tax rates are expected to be higher or lower than future tax rates

In other words, the best withdrawal source is not always the account with the highest balance or the account that feels most convenient. It is the account that best fits the broader tax and retirement income plan.

How Winding Trail Financial Planning Helps

Winding Trail Financial Planning is a fee-only financial planner in Lafayette, Colorado serving retirees and near-retirees in Boulder County and the greater Denver-Boulder area.

We help clients coordinate retirement income decisions across taxes, investments, Social Security, Medicare, and estate planning. For many households, that includes evaluating which accounts to draw from, when Roth conversions may make sense, how future required minimum distributions may affect taxes, and how to create a sustainable income plan that is not driven by rules of thumb.

Our work may include:

Year-by-year retirement tax projections

IRA, 401(k), Roth IRA, and brokerage withdrawal planning

Roth conversion analysis

Required minimum distribution planning

Social Security timing review

Medicare IRMAA awareness

Charitable giving strategies, including qualified charitable distributions

Coordination between investment management and tax planning

Surviving spouse tax planning

Because we are fee-only, our compensation comes from clients rather than commissions. That structure helps keep the focus on advice, planning, and implementation decisions that fit the client’s situation.

Why Work With a Fiduciary Retirement Planner?

A fiduciary retirement planner is obligated to put your interests first. That matters when retirement income decisions involve tradeoffs between investments, taxes, risk, income, and estate planning.

Tax-smart withdrawal planning should not be driven by a product sale or a generic rule of thumb. It should be based on your actual financial life.

For retirees and near-retirees in Lafayette, Boulder County, and the Denver-Boulder area, the planning process may include:

Reviewing all retirement and investment accounts

Mapping expected income sources

Estimating future required minimum distributions

Evaluating Roth conversion opportunities

Coordinating Social Security timing

Reviewing Medicare income thresholds

Planning charitable giving strategies

Creating a year-by-year tax projection

Coordinating with your tax return and investment strategy

The objective is to make better decisions before the tax consequences become unavoidable.

When Should You Start Planning?

The best time to build a retirement withdrawal strategy is often before retirement begins. In your 50s is a great time to start if you can.

You may benefit from tax-smart retirement income planning if:

You recently retired

You have large pre-tax IRA or 401(k) balances

You are deciding when to claim Social Security

You have taxable brokerage assets with gains

You are approaching required minimum distribution age

You are charitably inclined

You are concerned about Medicare premiums

You want your spouse to be financially secure if you die first

Even if you are already retired, it may not be too late to improve the strategy. Many retirees still have opportunities to manage income, taxes, account withdrawals, and long-term planning outcomes.

Final Thoughts

A strong retirement plan should do more than estimate whether you have enough money. It should also help you decide how to use that money wisely.

For retirees in Lafayette, Louisville, Eries, Boulder County, and the greater Denver-Boulder area, tax-smart withdrawal planning can help coordinate your IRAs, Roth accounts, brokerage assets, Social Security, Medicare premiums, and long-term estate goals.

The right withdrawal strategy is personal. It should be based on your income needs, your tax picture, your family situation, and your goals for the future.

A thoughtful plan can help you avoid unnecessary tax surprises, preserve flexibility, and make more confident retirement income decisions.

Thanks for reading.

Dwight Dettloff, CFP®, CPA/PFS, RICP®

The best retirement withdrawal strategy is not always the one that produces the lowest tax bill this year. It is the one that supports your income needs while managing taxes over time. If you want to understand how your accounts, Social Security, Roth conversions, and future RMDs fit together, a retirement tax planning review may be a good next step. Connect here.

FAQs

What is a tax-smart retirement withdrawal strategy?

A tax-smart retirement withdrawal strategy is a plan for deciding which accounts to draw from, how much to withdraw, and when to recognize taxable income. The goal is to support your retirement income needs while managing taxes over time.

Which retirement account should I withdraw from first?

There is no universal answer. Some retirees should use taxable brokerage assets first, while others may benefit from planned IRA withdrawals or Roth conversions. The best order depends on your tax bracket, Social Security timing, RMD outlook, Medicare premiums, estate goals, and cash flow needs.

Should I spend my taxable brokerage account before my IRA?

Sometimes. Taxable brokerage accounts can provide flexibility because withdrawals are not always taxed the same way as IRA distributions. Notably, planning in your 50s or a few years out from retirement might show that having additional taxable dollars can help with that optionality. However, automatically spending brokerage assets first may allow IRA balances to grow and create larger required minimum distributions later.

Are Roth conversions a good idea before retirement?

Roth conversions can be useful in lower-income years, especially after retirement and before required minimum distributions begin. But they need to be planned carefully because conversions increase taxable income in the year they are completed.

Can Roth conversions increase Medicare premiums?

Yes. Roth conversions can increase income used to determine Medicare IRMAA surcharges. That does not mean Roth conversions should always be avoided, but the potential Medicare impact should be considered before converting.

What are required minimum distributions?

Required minimum distributions, often called RMDs, are mandatory withdrawals from certain pre-tax retirement accounts after you reach the applicable RMD age. RMDs are generally taxable and can affect your broader retirement tax plan.

How does Social Security affect retirement withdrawal planning?

Social Security affects how much you need to withdraw from your portfolio and how much taxable income you may have. The timing of Social Security can also affect opportunities for IRA withdrawals or Roth conversions in lower-income years.

Why does the surviving spouse matter in retirement tax planning?

After one spouse dies, the surviving spouse may have similar income but file as a single taxpayer. This can create higher tax exposure. Planning ahead may help reduce future tax pressure on the surviving spouse.

Is tax-optimized withdrawal planning only for wealthy retirees?

No. Tax-smart withdrawal planning can be useful for many retirees who have multiple account types, including IRAs, 401(k)s, Roth IRAs, brokerage accounts, pensions, or Social Security. The more account types and income sources you have, the more valuable coordination may become.

Do Colorado retirees need a different withdrawal strategy?

Colorado retirees should consider both federal and state tax rules when creating a withdrawal strategy. Local cost of living, home equity, pensions, retirement account balances, and charitable goals can also affect the best approach.

How often should I review my retirement withdrawal strategy?

At least annually. Tax laws, investment markets, spending needs, health care costs, Medicare thresholds, and family circumstances can change. A withdrawal strategy should be updated as your life changes.

What is the difference between retirement income planning and investment management?

Investment management focuses on how your assets are invested. Retirement income planning focuses on how those assets are used to support spending, taxes, Social Security, Medicare, and estate goals. In retirement, these decisions should be coordinated.

Disclaimer:

The information provided herein was obtained from sources believed to be reliable and is believed to be accurate as of the time presented, but is without any express or implied warranties of any kind. Neither Winding Trail Financial Planning, LLC nor Dwight Dettloff warrant that the information is free from error.

The information provided herein is not advice specific to you or your circumstances but is instead general tips and education. None of the information provided herein is intended as investment, tax, or legal advice. Your use of the information is at your sole risk. Before considering acting on any information provided herein, you should consult with your investment, tax, or legal advisor. Under no circumstances shall Winding Trail Financial Planning, LLC or Dwight Dettloff be liable for any direct, indirect, special or consequential damages that result from your use of, or your inability to use, the information provided herein.

This information is not intended as a recommendation, offer or solicitation to buy, hold or sell any financial instrument or investment advisory services.

Disclaimer: None of the information provided herein is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement, of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. The content is provided ‘as is’ and without warranties, either expressed or implied. Winding Trail Financial Planning, LLC does not promise or guarantee any income or particular result from your use of the information contained herein. Under no circumstances will Winding Trail Financial Planning, LLC be liable for any loss or damage caused by your reliance on the information contained herein. It is your responsibility to evaluate any information, opinion, or other content contained.

Plan Your Next Chapter

Download our free guide "Seven Essentials for Successful Investing in Retirement" and get clarity on what really matters for your retirement success.