The Silent Retirement Risk: Why Inflation Can Be More Dangerous Than Market Volatility

When people think about the risks to their retirement plan, market crashes usually come to mind first.

That makes sense.

Market downturns are loud. They show up on the news, in your account statements, and in conversations with friends and family. If your portfolio drops 20% or 30%, you feel it immediately.

But there is another retirement risk that often receives less attention.

Inflation.

Inflation does not usually feel like a crisis in any single year. Groceries cost a little more. Insurance premiums creep higher. Property taxes, utilities, travel, home repairs, and healthcare expenses gradually increase.

None of those increases may seem dramatic by themselves.

But over a 20-, 25-, or 30-year retirement, inflation can become one of the most persistent and destructive threats to your financial plan.

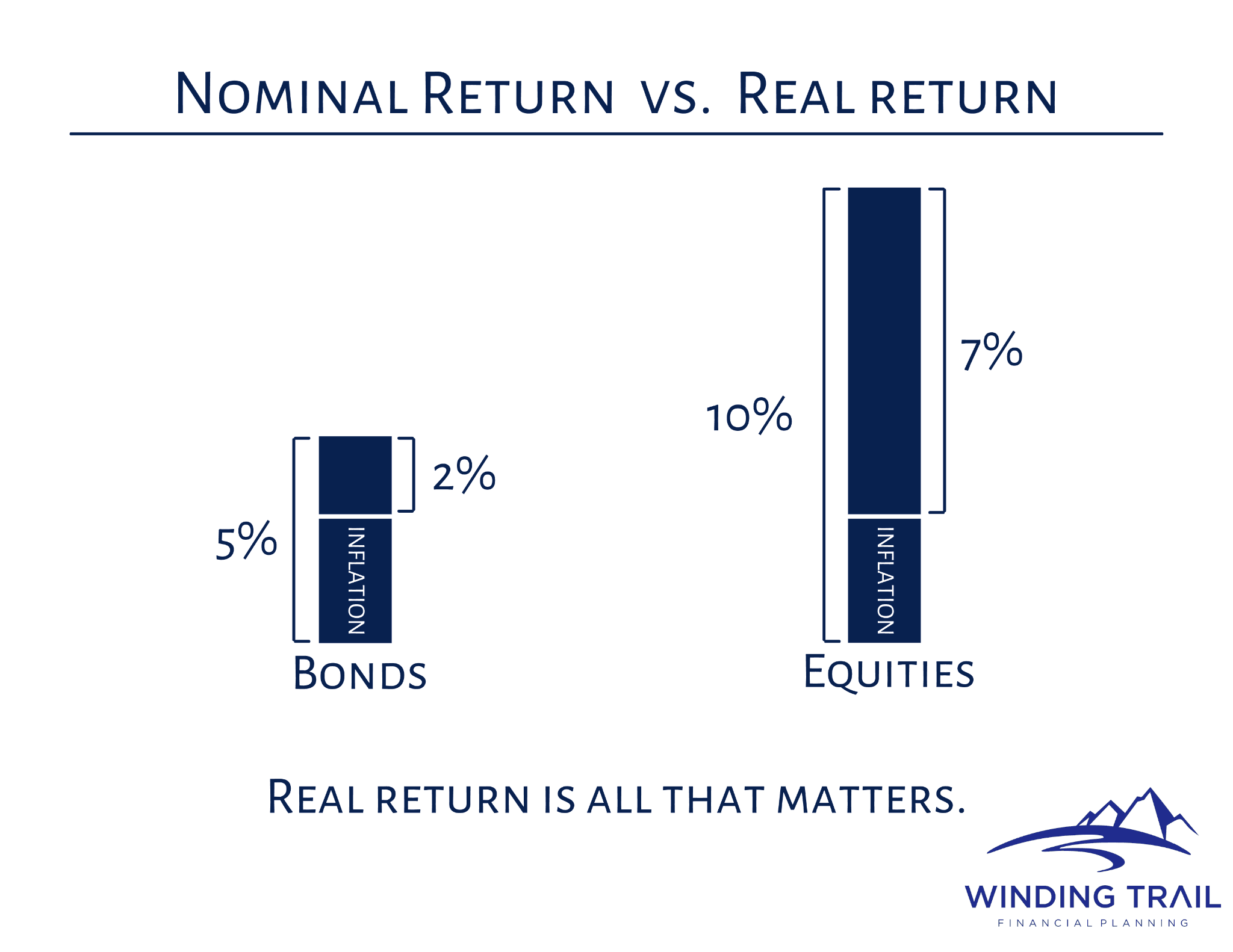

At a 3% annual inflation rate, prices roughly double in about 24 years. That means something that costs $5,000 per month today could cost close to $10,000 per month later in retirement, just to maintain a similar lifestyle.

If inflation runs closer to 4%, prices double even faster.

That does not mean every retiree’s spending will move in a perfectly straight line. Some expenses may go down as you age. Others, especially healthcare, insurance, taxes, housing, and home maintenance, may rise faster than general inflation.

But the broader point is important: a retirement income plan built around today’s expenses may not be enough for tomorrow’s reality.

That is why retirement planning is not just about avoiding market losses. It is also about protecting your purchasing power.

Why Inflation Matters So Much in Retirement

Retirement is not one moment in time.

It is a long period of life that may last 25 to 35 years, or more. A plan that looks safe at age 65 may feel much tighter at age 80 if income has not kept pace with rising costs.

This is why the years leading up to retirement are so important. If you are getting close, it may help to review what you should do 5 years before retirement, including your income plan, investments, taxes, Social Security, Medicare, and cash flow.

This is especially important for retirees who rely heavily on fixed income sources.

A pension that does not have a meaningful cost-of-living adjustment may feel comfortable in the first few years of retirement. But 15 or 20 years later, that same monthly benefit may not buy nearly as much.

The same can be true for annuities, bond interest, CDs, cash, or fixed-dollar portfolio withdrawals. These tools can all have a place in a retirement plan, but they do not automatically solve the inflation problem.

That is the tradeoff.

A retirement plan can look very safe on paper because it avoids short-term volatility. But if the plan does not include enough long-term growth, it may expose you to a different kind of risk: the risk that your income slowly loses purchasing power.

The Problem With Being Too Conservative Too Soon

As people get close to retirement, it is natural to want to reduce risk.

After all, you no longer have decades of employment income ahead of you. You may not want to ride through a major market downturn with the same portfolio you had in your 40s or early 50s.

That is reasonable.

The issue is when “reducing risk” turns into eliminating too much growth from the plan.

A portfolio that is almost entirely cash, CDs, short-term bonds, or fixed income may feel comfortable because the balance does not move around as much. But the real question is not just whether the account balance is stable.

The question is whether the portfolio can support your future spending after inflation.

This is where many retirees face a difficult balance.

Market volatility is visible and uncomfortable. Inflation is slower and easier to underestimate. But both are real risks.

The goal is not to take more investment risk than necessary. The goal is to take the right kinds of risk for the right time horizon.

This is also why financial planning in your 50s matters so much. You still have time to adjust your investment allocation, savings strategy, tax picture, and retirement income plan before the paycheck stops.

Why Retirees May Still Need Stocks

Stocks can be uncomfortable in retirement.

They go down. Sometimes by a lot. Sometimes at exactly the wrong time.

That is why retirees should not blindly own stocks without a plan for withdrawals, cash reserves, taxes, and risk management.

But avoiding stocks entirely can create its own problem.

Over long periods of time, stocks have historically provided returns that exceed inflation. Businesses can raise prices, grow earnings, pay dividends, and participate in the broader growth of the economy. While none of that happens in a straight line, equities have historically been one of the primary ways investors have preserved and increased purchasing power over long periods.

That matters because retirement is not a short-term goal.

Even if you retire at 65, part of your portfolio may be designed to support spending at age 75, 80, 85, or 90. Money that you do not need for 10, 15, or 20 years has a very different time horizon than money you need over the next 12 months.

That does not mean every retiree needs the same stock allocation.

Some people have large pensions. Some have rental income. Some have significant Social Security benefits. Others rely heavily on their investment portfolio for spending.

But for many retirees, some exposure to equities remains an important part of protecting long-term purchasing power.

Bonds Still Have a Role

None of this means bonds are bad.

In fact, bonds, cash, CDs, and other more conservative investments can be very useful in retirement. They can provide stability, liquidity, income, and a source of funds during market downturns.

The issue is not whether retirees should own bonds.

The issue is whether the overall plan has enough growth to keep up with rising costs.

A well-built retirement portfolio often uses safer assets for near-term spending needs and growth assets for longer-term needs. This can help reduce the risk of selling stocks during a downturn while still giving the plan a chance to outpace inflation over time.

That balance is the key.

Too much volatility can make retirement stressful. But too little growth can make retirement financially fragile later on.

Inflation Does Not Affect Every Retiree the Same Way

Inflation does not hit every household equally.

For example, Social Security includes cost-of-living adjustments, which can help retirees keep up with inflation. That is one reason Social Security can be such a valuable part of a retirement income plan.

Some pensions also include cost-of-living adjustments, but many do not. Others may have partial adjustments or caps that do not fully match actual inflation.

Housing also matters.

A retiree with a fixed-rate mortgage or a paid-off home may have different inflation exposure than someone who rents. However, even homeowners are not immune. Property taxes, insurance, utilities, HOA dues, maintenance, and repairs can all increase over time.

Housing is one reason the decision to pay off your mortgage before retiring in Colorado should be evaluated in the context of cash flow, liquidity, taxes, investment risk, and peace of mind.

Healthcare is another major factor.

Medicare premiums, supplemental insurance, prescription drugs, dental care, long-term care, and out-of-pocket medical costs can all become more important later in retirement. Even retirees who spend less on travel or entertainment as they age may spend more on healthcare-related needs.

Taxes can also play a role.

If more of your retirement income comes from pre-tax accounts like traditional IRAs and 401(k)s, rising withdrawals may also mean higher taxable income. Required minimum distributions can add another layer of complexity later in retirement.

For Colorado retirees, it is helpful to understand what taxes retirees may pay in Colorado, including how Social Security, pensions, IRA withdrawals, Roth accounts, property taxes, and investment income may fit together.

This is why inflation planning should not happen in isolation. It should be connected to your investment strategy, tax plan, Social Security decision, withdrawal strategy, and estate plan.

How to Build Inflation Protection Into a Retirement Plan

There is no single perfect way to protect a retirement plan from inflation.

But there are several practical planning decisions that can help.

First, maintain an appropriate amount of growth in the portfolio. For many retirees, this means continuing to own some stocks or stock funds, even after retirement. The right amount depends on your spending needs, risk tolerance, income sources, and overall financial picture.

Second, avoid holding too much long-term money in cash. Cash is important for emergencies and near-term spending. But cash that sits for years may lose purchasing power if interest rates do not keep up with inflation after taxes.

Third, use a flexible withdrawal strategy. Taking the same inflation-adjusted withdrawal every year may not always make sense. In some years, it may be appropriate to increase spending. In others, especially after difficult market years, it may be wise to temporarily slow withdrawals or use other income sources. For many households, this is where tax-smart retirement withdrawals become important.

Fourth, coordinate Social Security carefully. Since Social Security benefits receive cost-of-living adjustments, the claiming decision can have a major impact on inflation-protected income over a long retirement. Delaying benefits is not always the right answer, but it should be evaluated thoughtfully.

Fifth, plan for taxes. Inflation can increase the dollar amount you need to withdraw, but taxes determine how much of that withdrawal you actually keep. This is one reason it is worth reviewing common retirement tax planning traps before you retire, especially if you have large pre-tax IRA or 401(k) balances. Roth conversions, tax-efficient withdrawals, charitable giving strategies, and capital gain planning may all affect how much after-tax income you have available to spend.

Finally, revisit the plan regularly. Inflation assumptions, investment returns, tax laws, spending needs, and life circumstances all change. A retirement plan should not be built once and then ignored.

Retirement Income Should Be Able to Adapt

A good retirement income plan is not just about creating a paycheck for the first year of retirement.

It is about creating a system that can adapt.

Your spending will change. Markets will change. Tax laws will change. Interest rates will change. Inflation will change.

That is why the plan should include both stability and flexibility.

Stability matters because retirees need confidence. You need to know where your near-term income is coming from. You need enough conservative assets to avoid being forced to sell stocks during every market downturn.

But flexibility matters too.

If your income plan is too rigid, it may not handle inflation well. If your portfolio is too conservative, it may not grow enough. If your withdrawals are too fixed, they may not adjust well to changing market conditions or tax opportunities.

Retirement planning is less about finding one perfect answer and more about building a framework that can handle uncertainty.

The Silent Threat Deserves More Attention

Market crashes will always get more attention than inflation.

They are sudden. They are emotional. They dominate headlines.

Inflation works differently. It moves gradually, often in ways that are easy to dismiss in the moment. But over a long retirement, it can have a major impact on your financial security.

A dollar today will not buy the same amount 20 or 30 years from now. Your retirement plan should reflect that reality.

That does not mean taking unnecessary risk. It means understanding the risks you are already taking, whether they show up as market volatility, inflation, taxes, healthcare costs, or reduced flexibility.

The goal is not simply to avoid short-term losses.

The goal is to maintain your lifestyle, preserve your purchasing power, and create a retirement income plan that can support you for the long haul.

Thanks for reading!

-Dwight Dettloff, CFP®, CPA/PFS, RICP®

Final Thoughts

Inflation may not feel as scary as a market crash, but it can be just as important to plan for.

For retirees and near-retirees, the challenge is balancing the need for stability today with the need for growth tomorrow. A retirement plan that avoids volatility but fails to keep up with rising costs may not be as safe as it appears.

Winding Trail Financial Planning is a fee-only financial advisor in Lafayette, Colorado. We help retirees and near-retirees build tax-aware retirement income plans that account for market risk, inflation, Social Security, taxes, and long-term spending needs.

If you are within a few years of retirement and want help thinking through how inflation could affect your income plan, you can schedule a time to talk.

Frequently Asked Questions About Inflation and Retirement

How does inflation affect retirement income?

Inflation reduces the purchasing power of your retirement income over time. If your expenses rise but your income stays flat, the same monthly income may buy less later in retirement.

Why do retirees still need stocks?

Many retirees still need some exposure to stocks because retirement can last several decades. Stocks can be volatile in the short term, but they may help a portfolio grow enough to keep up with inflation over time.

Are bonds bad for retirees during inflation?

No. Bonds can still provide stability, income, and liquidity. The risk is relying too heavily on fixed-income investments if they do not provide enough long-term growth to preserve purchasing power.

Does Social Security protect against inflation?

Social Security includes cost-of-living adjustments, which can help retirees keep up with inflation. However, Social Security may only cover part of a retiree’s total spending needs.

What is one way to protect a retirement plan from inflation?

One strategy is to combine stable income sources with growth-oriented investments, while using a flexible withdrawal plan that can adjust over time.

Disclaimer: None of the information provided herein is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement, of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. The content is provided ‘as is’ and without warranties, either expressed or implied. Winding Trail Financial Planning, LLC does not promise or guarantee any income or particular result from your use of the information contained herein. Under no circumstances will Winding Trail Financial Planning, LLC be liable for any loss or damage caused by your reliance on the information contained herein. It is your responsibility to evaluate any information, opinion, or other content contained.

Plan Your Next Chapter

Download our free guide "Seven Essentials for Successful Investing in Retirement" and get clarity on what really matters for your retirement success.